7.16.26 Imagining the Unthinkable for AI Investors

The most dangerous investment mistakes often begin with an inability to imagine outcomes that differ from what the market expects. That does not mean investors should reflexively bet against strong trends, because momentum is real and great businesses can stay great for a long time, but when an investment thesis depends on outcomes that are inherently unknowable, imagination becomes a risk-management tool.

One useful exercise is steel-manning, which is simply taking the other side of an argument or debate and building the strongest version of it. Perhaps the most uncomfortable version of that exercise is imagining a future in which today’s seemingly unquenchable AI data center and compute demand falls dramatically.

That sounds implausible in 2026. AI infrastructure remains one of the most powerful capital spending cycles in the world. A recent industry forecast from Gartner predicts global data center electricity consumption will rise 26% in 2026 to 565 TWh, with AI-optimized servers accounting for 31% of that consumption and exceeding conventional server power draw by 2027. Also from Gartner, worldwide AI spending is forecast at $2.59 trillion in 2026, up 47% year over year, with AI infrastructure representing more than 45% of spending.

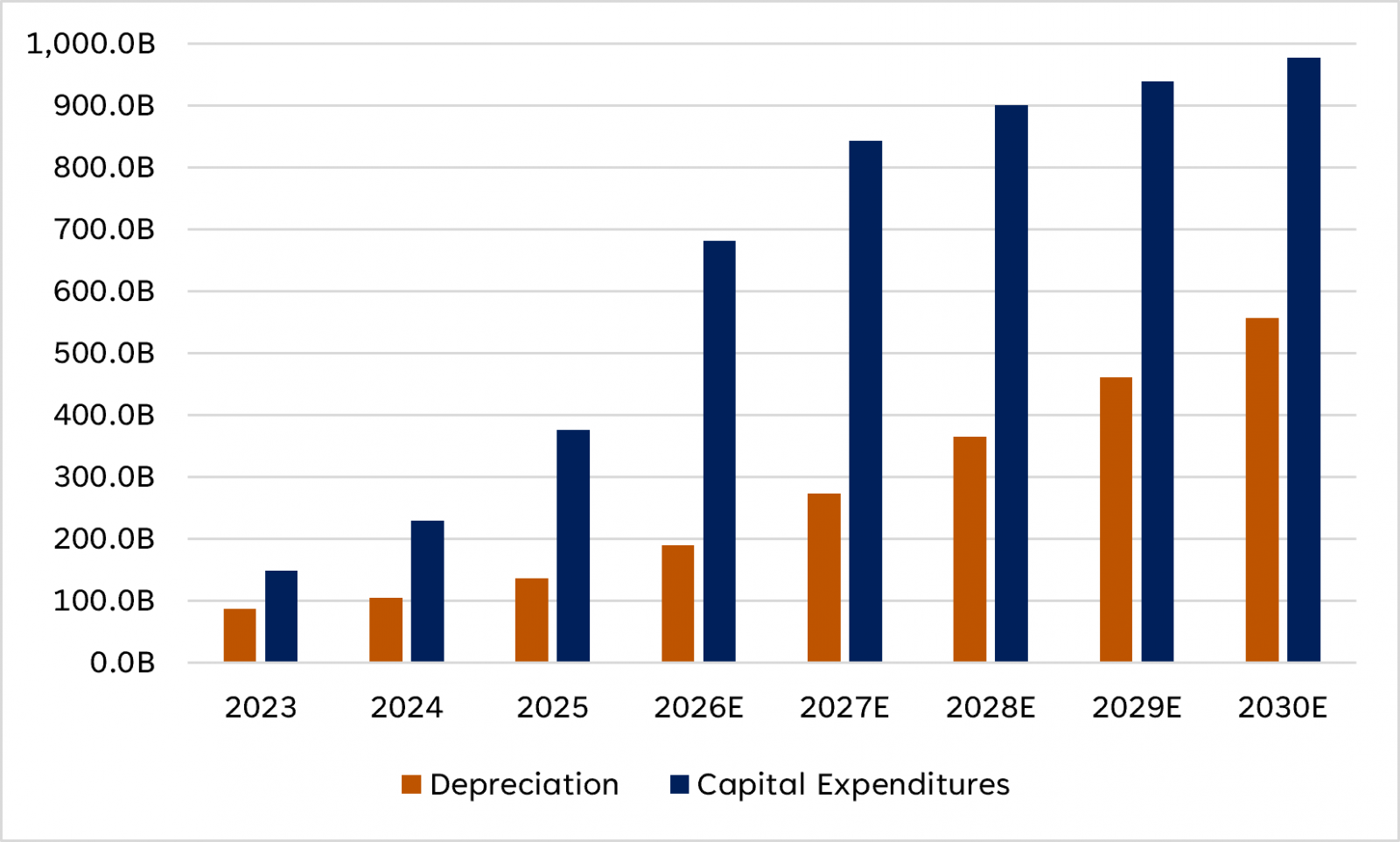

Hyperscaler Capital Expenditure and Depreciation History and Consensus Estimates 2023 – 2030E

- Source: Bloomberg 7/15/2026

- Disclosures: Past performance is no guarantee of future results. Estimates may not materialize as predicted and are subject to change.

This is exactly why the exercise matters. The more obvious a theme becomes, the more important it is to ask what could go wrong.

Imagine the following:

The year is 2035. GPU-filled "AI data centers" are running at 50% utilization, up slightly from 2030 but still miles below the 90%+ levels seen during the supply-constrained buildout years of 2026–27. Vast amounts of new capacity came online just as gains in model training plateaued, while inference costs kept climbing, thanks to a combination of monopolistic behavior among East Asian semiconductor fabs and nationalistic policies on both sides of the Pacific that kept capable, abundant, low-cost Chinese chips largely out of global markets. The result: the vast majority of the Fortune 500 realized minimal to no efficiency benefits relative to what they spent. Broad consumer large language models (LLMs), like ChatGPT, continue to bleed money, with free tiers still serving 95% of users. Advertising revenue has kept these "frontier model application" companies shambling along in a quasi-zombie state, trimming losses just enough each year to keep the dream alive. The one sector in which LLMs have undeniably proven their worth is fast food restaurants: it turns out the only place people genuinely prefer talking to a robot is the drive-thru.

We have no idea whether this made-up, hypothetical scenario is at all likely, but it is possible enough to analyze. Especially the bit about the drive-thru.

Fast food jokes aside, the capital-cycle risk is straightforward. Based on consensus estimates, the four largest hyperscalers will have spent over $4 trillion in capex from 2025 through 2030. Assuming half of that is related to AI and a roughly 20% annual depreciation rate on those assets, that implies about $400 billion of annual depreciation expense, greater than the group’s combined profits in 2025. This depreciation math is reflected in consensus estimates. Total hyperscaler depreciation in 2030, inclusive of non-AI business lines, is expected to be over $550 billion. If capacity is built, accounting costs eventually arrive, even if revenue disappoints. Servers, GPUs, buildings, power equipment, and networking assets depreciate on different schedules, meaning today’s income statements may not fully reflect tomorrow’s cost burden.

What about demand? OpenAI reportedly crossed 900 million weekly active users in 2026 and reached $25 billion in annualized revenue by February 2026. The monetization math is more uncertain, with approximately 50 million paying subscribers against 900 million weekly active users. The implication being that the overwhelming majority of usage remains free or lightly monetized. If consumer willingness to pay remains limited, and enterprise productivity benefits prove narrower or slower than expected, the industry may discover that usage is not the same thing as profitable demand.

There is also the possibility that AI becomes more efficient rather than endlessly more compute-intensive. After DeepSeek’s R1 release in January 2025, hyperscalers largely reaffirmed or increased spending plans, arguing that cheaper AI would expand use cases and therefore increase aggregate compute demand. This is the “Jevons Paradox” argument. That may be right, but steel-manning requires asking the opposite: what if a future model is not 20% more efficient, but 100x more efficient? What if the next architecture dramatically reduces inference costs and makes today’s data center buildout look oversized?

If something like the 2035 scenario materialized, the industry implications would be severe. GPU suppliers would face order digestion and margin compression. Data center developers would be left with underutilized capacity. Utilities and grid equipment suppliers might still benefit from a broader electrification cycle, but the AI-specific urgency embedded in valuations would fade. Hyperscalers would face a harder question. Were they investing to build a durable competitive advantage, or were they trapped in an arms race where the benefits ultimately accrued to customers? This outcome has played out time and time again. Most recently, the fiber laid during the dot-com boom ultimately helped create the modern internet, while the returns on those investments certainly disappointed.

Is our imagination too pessimistic? Perhaps. But for long-term investors, we see a steel-man exercise like this as simply good discipline. When everyone is expressing crystal-ball level confidence in the future, a bit of contrarian imagination can point your analytical attention in a less-traveled direction. It also serves as a useful reminder that in capital-intensive booms, returns on investment typically disappoint.

Much of the narrative around AI today centers around its impact. That narrative and debate isn’t going anywhere: Is AI akin to the next industrial revolution? Is AI as important a technological development as electricity? Is AI simply the next evolution in computer capabilities, like the microprocessor or the graphical user interface? But the most important question for investors is not the magnitude of a technology’s societal impact. It is who earns the economics, over what time frame, and after how much capital has been spent to find out.

-

Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

For Public Use – Tracking: #1140952