7.14.26 What We Know About the Fed’s Task Forces

The Changing of the Guard

Kevin Warsh, the new chair of the Federal Open Market Committee, has an initiative to modernize the way policy is developed, and he has established five task forces to evaluate the current process and deliver recommendations for improvement.

He framed the initiative around a simple reality: the U.S. economy looks very different today than it did a generation ago. With rapid technological change and shifting labor market dynamics, the Federal Reserve (Fed) is undertaking a broad review of how it conducts monetary policy. The five task forces have been charged with examining whether the central bank's analytical tools, policy frameworks, communications strategy, and operating procedures remain fit for purpose. By bringing together leading economists, former policymakers, business executives, and technology experts, the Fed appears intent on challenging conventional thinking and identifying ways to improve its decision-making process.

The Five Task Forces

Here is what we know about the leaders of these committees and their published views.

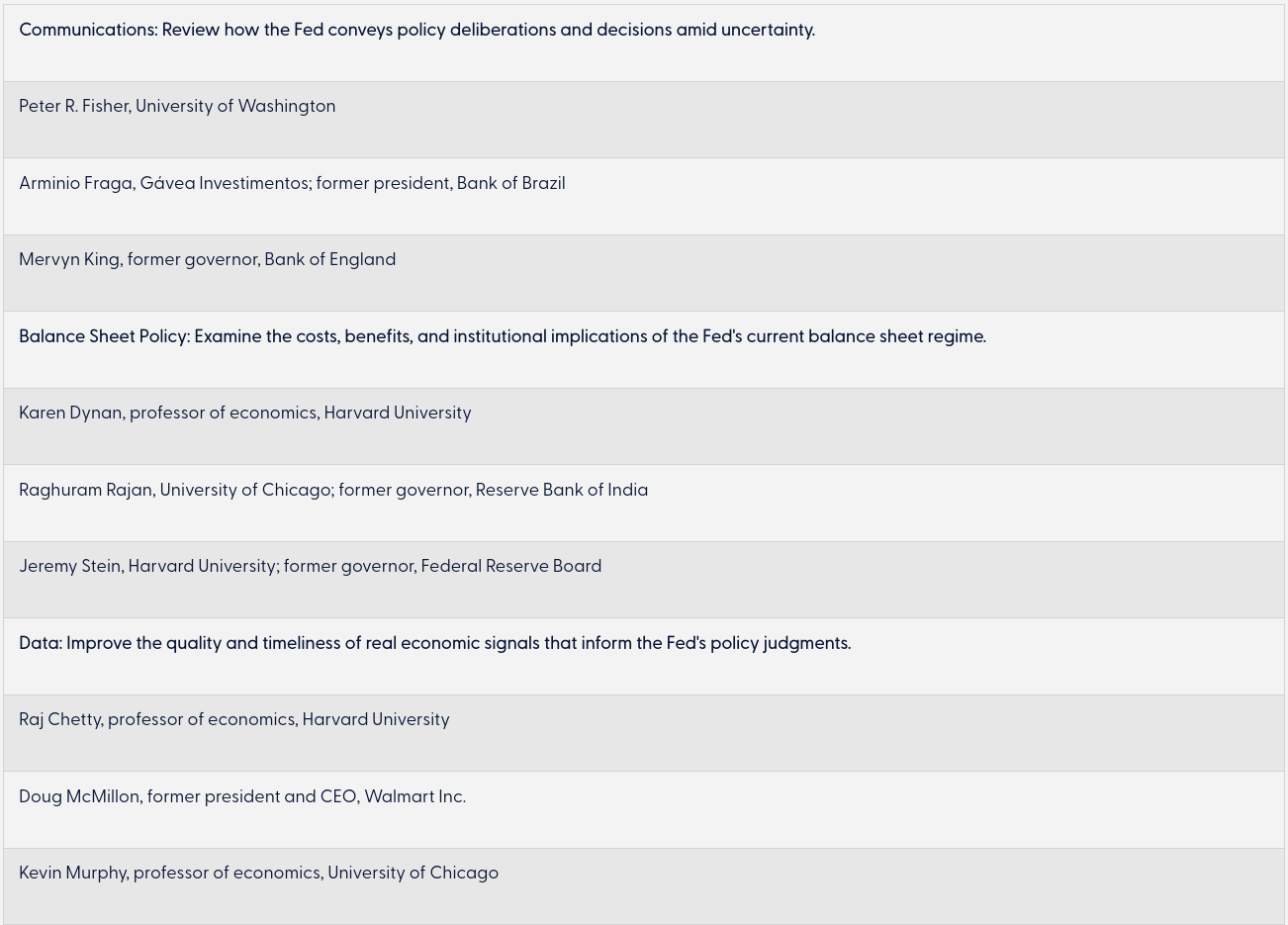

The composition of the Communications Task Force suggests a strong push toward greater clarity and realism in how the Fed communicates in uncertainty. Peter Fisher has long argued that central banks should be careful about creating false confidence through overly precise guidance, while Mervyn King has criticized the tendency of central banks to imply they possess more knowledge than they actually do. Arminio Fraga brings an emerging-market central banking perspective where credibility is earned through consistent actions rather than elaborate forward guidance. As a result, this group is likely to recommend simplifying Fed communications, reducing the reliance on detailed forward guidance, and placing greater emphasis on explaining risks, alternative scenarios, and uncertainty surrounding forecasts.

The Balance Sheet Policy Task Force appears likely to take a more skeptical view of the very large balance sheet that has characterized the post-financial-crisis era. Raghuram Rajan has frequently warned about unintended consequences from prolonged monetary accommodation and distortions created by abundant liquidity. Jeremy Stein has conducted influential research on financial stability risks arising from credit markets and investor behavior, while Karen Dynan brings a more pragmatic, evidence-based macroeconomic perspective. Collectively, the group is unlikely to advocate an abrupt retreat from quantitative easing tools, but it may recommend a smaller long-run balance sheet, a clearer framework for emergency asset purchases, and greater attention to financial stability considerations when deploying unconventional policies.

The Data and Productivity and Jobs Task Forces point toward a Fed that relies more heavily on real-time private-sector information and places greater weight on supply-side developments. Raj Chetty has pioneered the use of high-frequency administrative and private-sector data, while Doug McMillon's retail background provides direct insight into consumer spending patterns and pricing behavior.

At the same time, the inclusion of Marc Andreessen, Charles Jones, and Asha Sharma signals a strong interest in understanding how artificial intelligence and other general-purpose technologies could raise productivity growth and reshape labor markets. These groups will likely encourage the Fed to supplement traditional government statistics with real-time indicators and to devote greater resources to measuring technological change, labor reallocation, and productivity gains that may alter the economy's speed limit.

The Inflation Frameworks Task Force may ultimately produce the most consequential recommendations. Greg Mankiw, Thomas Sargent, and William White all have reputations for taking inflation risks seriously, albeit from different perspectives. Sargent's work emphasizes expectations and policy credibility, while White has repeatedly warned about the dangers of maintaining excessively easy monetary conditions, and Mankiw has generally favored practical, rules-based approaches to monetary policy. Given this lineup, the task force may recommend moving away from frameworks that tolerate prolonged overshoots of inflation, placing greater emphasis on inflation expectations and money and credit conditions, and adopting a more systematic approach to policy decisions.

Conclusion

Looking across the five task forces, the composition of the groups suggests that Fed leadership is seeking a fresh assessment of many of the assumptions that have guided monetary policy over the past two decades. The emphasis appears to be on stronger empirical analysis, better real-time data, a deeper understanding of supply-side forces, such as productivity and technology, and a renewed focus on institutional credibility. Taken together, the appointments hint at a review process that is likely to question the effectiveness of highly interventionist policy approaches and explore whether a more disciplined and durable framework can better support the Fed's long-run objectives of price stability and maximum employment.

-

Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

For Public Use – Tracking: #1139560