6.4.26 Oil Market Underestimates Frictions Beyond a Deal

For weeks now, media reports have been suggesting that Washington and Tehran are moving closer to a memorandum of understanding (MOU). In practical terms, that would extend the current ceasefire by roughly 60 days and create a window to negotiate a more durable peace agreement. The market’s constructive read is straightforward: an MOU should allow flows through the Strait of Hormuz to stabilize quickly, if not normalize outright very soon.

We think that interpretation is a bit too linear. Even if an MOU is signed, it does not automatically translate into an immediate surge in oil supply. The more realistic near-term path is incremental. Any early increase in barrels is likely to come from already-produced crude, including crude sitting on stranded or floating vessels and Iranian cargoes in storage, rather than a sustained restart in production or exports. In other words, this is more about clearing existing bottlenecks than reflating the supply base. At the same time, the market appears to be underestimating the logistical challenges. Tankers have been repositioned globally over the past two months, insurance premia have adjusted materially higher, and operational risk remains elevated. Getting flows back up is not as simple as flipping a switch. Shipowners and insurers will need clarity that vessels can safely transit into and out of the region before meaningfully committing capacity. With residual risks around mines, miscalculation, or a relapse in hostilities, that confidence is unlikely to be rebuilt overnight.

Bigger picture, a more meaningful and sustained recovery in supply likely requires something far more comprehensive than an interim MOU. A full agreement between the U.S. and Iran remains a high bar, with clear gaps still in place across core issues like nuclear constraints, sanctions relief architecture, and the longer-term framework governing transit through Hormuz. These are complex, interconnected issues, and even under best-case assumptions, they are unlikely to be resolved quickly. Realistically, the process could absorb much, if not all, of the proposed 60-day window, pushing us closer to peak summer driving season in the U.S. Crucially, the negotiation phase is unlikely to be smooth. The same complexity that makes a final deal so difficult to achieve also increases the risk of periodic setbacks or flare-ups along the way. Markets tend to discount outcomes; they are less efficient at pricing path dependency. Here, the path matters as any disruption will quickly affect sentiment and flows.

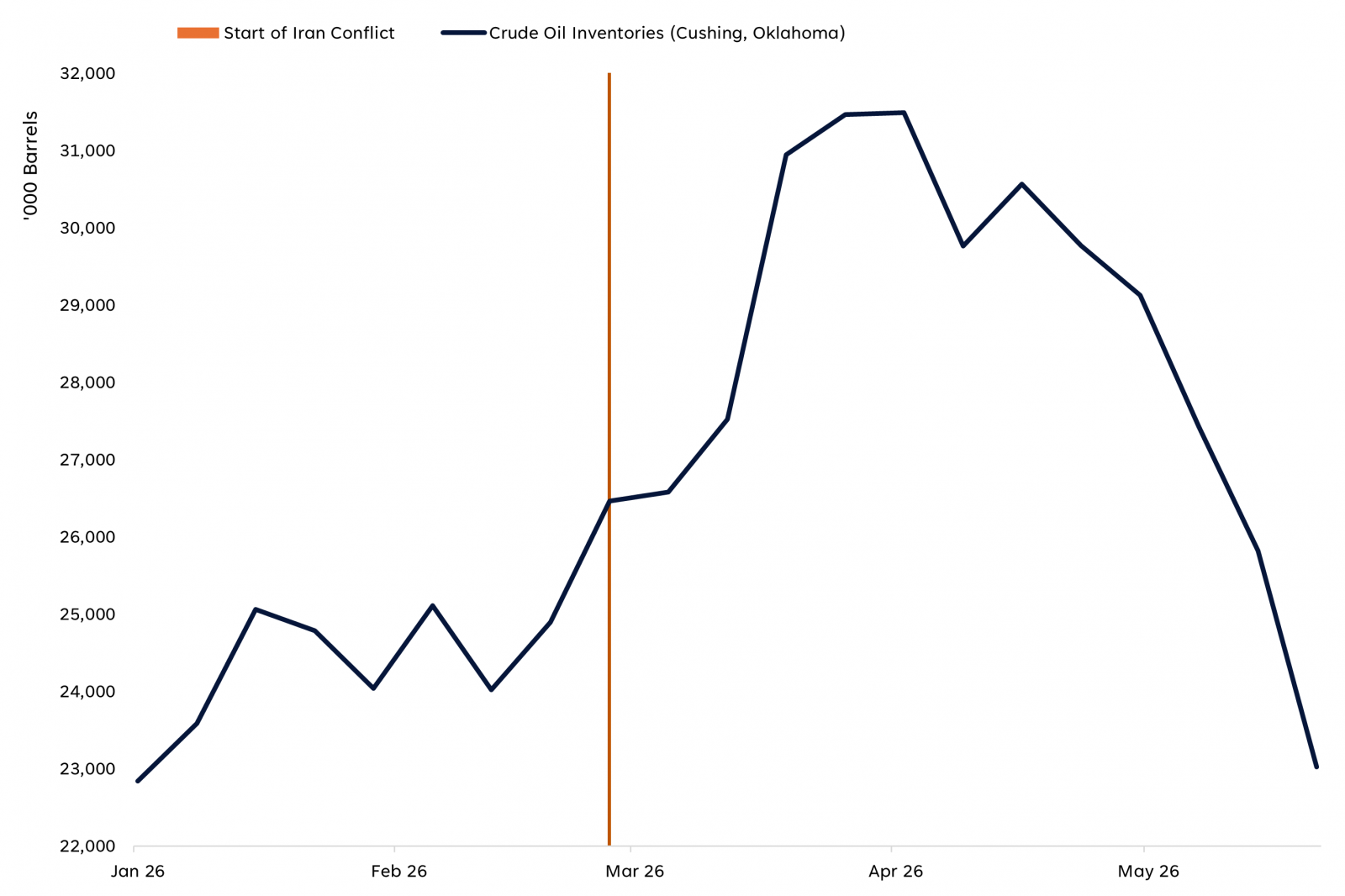

Cushing Inventories on Track to Reach Critical Lows Within Weeks

Source: LPL Research, U.S. Department of Energy, Bloomberg 06/03/26

Disclosure: Past performance is no guarantee of future results.

Meanwhile, the underlying physical backdrop remains tight. Inventories continue to draw at a steady clip and will only keep declining in the event of a prolonged negotiation period. Against that backdrop, the near-term risk profile for crude prices still appears skewed to the upside, in our view. For that outlook to shift in a meaningful way, we would need to see not only a near-term MOU but also clear and tangible progress toward a broader agreement that more permanently restores shipping flows closer to normal levels. At this stage, market participants appear to be getting somewhat ahead of themselves, with pricing reflecting a degree of conviction that may not yet be fully supported by actual developments.

-

Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

For Public Use – Tracking: #1119572