6.30.26 What to Watch This Earnings Season

The second quarter wraps up today, and it was a good one. With the S&P 500 having returned more than 14% (including dividends) with just one trading day left, it will almost certainly end up being the best quarter for the index since the second quarter of 2020. Technology was the leader despite the June weakness.

As the quarter ends, corporate America closes its books and prepares to report results to the public over the coming months. First quarter results were spectacular, as S&P 500 companies collectively grew earnings per share (EPS) by 29%. Even excluding private equity gains on OpenAI and Anthropic shares held by mega-cap technology companies, we estimate last quarter’s earnings were up over 20%. Will companies deliver another blockbuster?

If earnings growth is going to again approach 30% — very possible with consensus estimates calling for 23% — the technology sector will have to do more heavy lifting. Memory chip maker Micron (MU) did its part by growing earnings 12x and contributing to 4.5 points of S&P 500 EPS growth by itself. In fact, MU and NVIDIA (NVDA) are expected to drive 40% of overall S&P 500 EPS growth and, according to Goldman Sachs estimates, artificial intelligence (AI) infrastructure stocks are expected to contribute 60% of S&P 500 EPS (the technology sector is expected to contribute a similar amount). Besides technology, only energy, at 5.0%, is expected to contribute more than one point of S&P 500 EPS growth.

That strength from tech may not be surprising if you’ve been following earnings in recent quarters. What might surprise you, though, is that S&P 500 EPS growth excluding the Magnificent Seven — bolstered by the memory makers — was 17.5% in the first quarter and is expected to eclipse 20.5% in the second quarter (Q2).

S&P 500 Earnings Growth Excluding the Magnificent Seven May Exceed 20% in Q2

- Source: LPL Research, Bloomberg 06/29/26

- Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results. Estimates may not materialize as predicted and are subject to change.

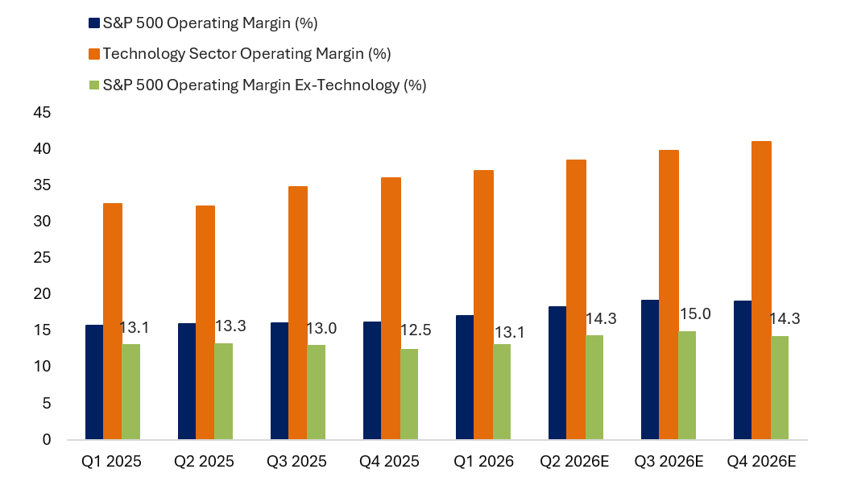

Ramp-up of Profit Margins is Equally Impressive

If earnings are going to hit consensus estimates in Q2 and the second half, margins will have to expand quite a bit — enough to convert low-teens revenue growth into at least double that pace of earnings growth. As shown in the “Profit Margin Expansion is Not Just a Technology Story” chart, margins excluding technology are on the way up. The productivity from AI should increasingly show up in the form of higher profit margins in the second half of 2026. Lower tariffs will also be helpful, although higher memory chip prices and energy and other bottlenecks in the Strait of Hormuz could erode company margins, particularly in the technology sector.

Profit Margin Expansion is Not Just a Technology Story

- Source: LPL Research, Bloomberg 06/29/26

- Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results. Estimates may not materialize as predicted and are subject to change.

Conclusion

The AI boom should drive another quarter of S&P 500 EPS growth near 30% when all results are in. The boost to oil prices from the Iran conflict will enable energy to chip in, but technology is expected to do most of the work. Like last quarter, investors will want to see returns on the massive AI investment. Margins will be closely watched, as they face several crosscurrents and are key to potentially keeping up this torrid pace of earnings growth as corporate America seeks out AI productivity gains.

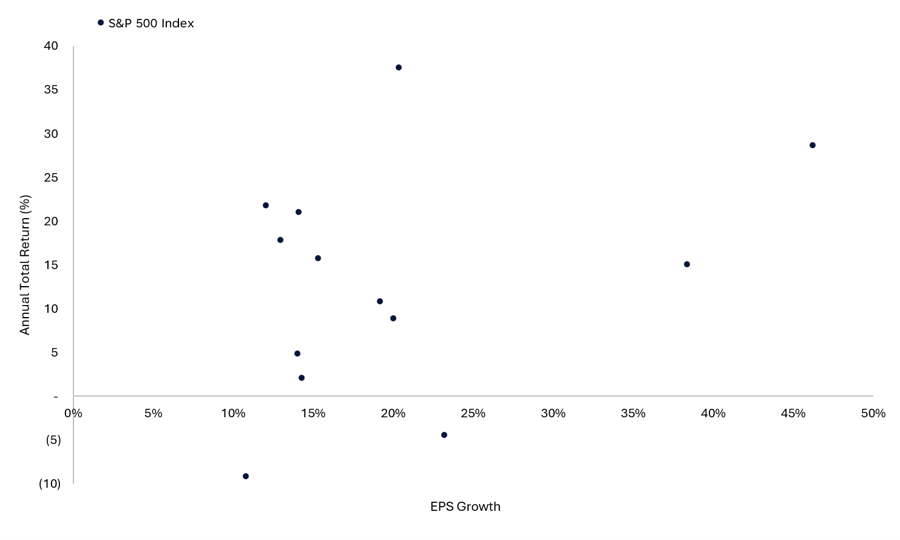

History is clear on the rewards for strong earnings, because when S&P 500 earnings grow double-digits, the average annual S&P 500 index return is 14.3% with gains in 10 of the past 12 years. This year should make it 11 out of 13. The bursting of the dot-com bubble in 2000 and the Fed rate hike scare of 2018 were the only two years since 1990 when the S&P 500 was down despite double-digit earnings growth.. Although it is important to remember that past performance does not guarantee future results.

Double-Digit Earnings Growth Years Tend to Be Strong Ones for Stocks

- Source: LPL Research, Bloomberg 06/29/26

- Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.2003 was omitted as an outlier with annual EPS growth of 362.3% and an annual total return of 28.7%. Current year is shown on table based on year-to-date performance and earnings estimates.

-

Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

For Public Use – Tracking: #1132969