5.14.26 Tactical Update: Rising Conviction on Earnings Growth

Rising Conviction on Earnings Growth

In last month’s update, we highlighted a shift from preparation to action as market conditions began to support increased equity exposure. Since then, that positioning has become even more grounded in fundamentals, as earnings have demonstrated strong growth. The improved backdrop also reflects an economy that continues to grow at a solid pace and a market that has remained resilient through recent geopolitical uncertainty.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) recently upgraded equities to overweight (by adding to small cap value), while trimming fixed income to underweight (via a reduction in mortgage-backed securities). That move reflects growing confidence in both the economic backdrop and the earnings outlook. Equity market leadership has remained concentrated in growth and large cap stocks, particularly within the technology sector, where continued investment in artificial intelligence (AI) is driving strong earnings trends. This leadership also reflects the scale of AI-related investment, which is disproportionately benefiting large cap companies with the balance sheet strength to fund that growth.

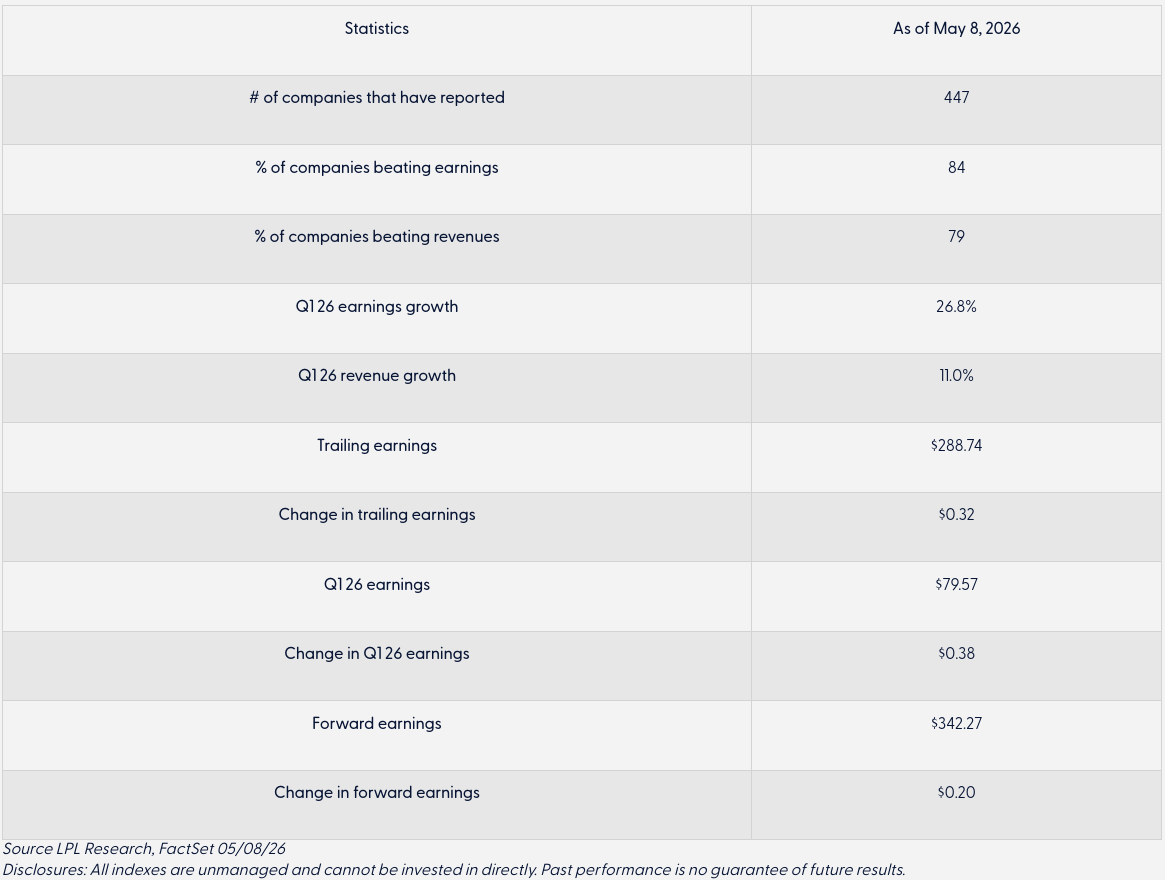

This earnings season has helped validate that view. As shown in the LPL Research Earnings Season Dashboard below, first quarter results have come in notably strong. Earnings growth is tracking at a torrid pace; a high percentage of companies are beating both earnings and revenue expectations, and forward estimates continue to move higher even late in the reporting cycle. Much of that strength is coming from the largest technology companies (the Magnificent Seven (Mag Seven) stocks have seen an average 57% earnings per share growth in Q1), but the overall tone of the season has been constructive. The average overall S&P 500 upside surprise has been strong, supported by communications services, consumer discretionary sectors, and semiconductors, while both earnings and revenue beat rates are running well above average. Forward estimates have also continued to rise in recent weeks, reflecting resilient demand and continued investment trends.

Earnings Season Dashboard

One of the most important dynamics in equity markets this year has been the relationship between prices and earnings. While the S&P 500 price has moved higher, earnings expectations (as measured by forward earnings per share (EPS)), have increased at a faster rate. The result is a modest decline in valuation multiples (as measured by the forward price to earnings (P/E) ratio, leaving the market somewhat “cheaper” today on a forward basis than it was at the start of the year. That is not something typically experienced during an equity rally to new all-time highs.

Year-To-Date Change in S&P 500 Price, Earnings, and Valuation

- EPS = Earnings Per Share, P/E = Price to Earnings Ratio

- Source LPL Research, Goldman Sachs GIR, FactSet 05/13/26

- Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

At the same time, it must be considered that earnings strength has been relatively concentrated, with a narrow group of companies driving both earnings revisions and market performance. That type of setup can lead to periods of volatility, particularly in momentum-oriented areas of the market, as leadership rotates beneath the surface.

Current Tactical Positioning

The STAAC’s recommended tactical asset allocation (TAA) includes an overweight stance toward U.S. equities. With a path to reduced geopolitical risk emerging and a supportive earnings backdrop, we expect equities to continue to find support. The STAAC maintains a preference for growth over value and slightly favors large caps over small caps, reflecting both earnings leadership and balance sheet strength. Continued investment in AI also reinforces that bias.

Fixed income remains less compelling in the near term, as yields are expected to remain rangebound and persistent inflation pressures may delay the timing of Federal Reserve rate cuts. In that environment, the return potential for bonds may be more limited relative to equities. At the same time, with economic and policy uncertainty likely to persist, we believe alternative investments can continue to play a role in helping manage portfolio volatility and improving diversification.

-

Important Disclosures

-

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

-

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

-

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

-

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

-

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

-

Asset Class Disclosures –

-

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

-

Bonds are subject to market and interest rate risk if sold prior to maturity.

-

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

-

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

-

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

-

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

-

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

-

Precious metal investing involves greater fluctuation and potential for losses.

-

The fast price swings of commodities will result in significant volatility in an investor's holdings.

-

This research material has been prepared by LPL Financial LLC.

-

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

-

Tracking: #1108759