4.8.26 Long-Term Opportunities Always Present Themselves

Early in my career, during a particularly challenging market environment, a mentor remarked that there are always opportunities — you simply have to look for them. That observation has remained a key tenet of my investment philosophy, particularly during periods of increased volatility.

Market sell-offs are disruptive and often heighten investor uncertainty. We have recently experienced one of those periods because of the ongoing war in the Middle East. Oil prices have surged and the S&P 500, at its March lows, has declined 9% from its all-time high set in February.

But improved market fundamentals might be creating some of those opportunities that tend to present themselves during periods like this one.

Concerns About the Future Path of Economic Growth

Expectations for the future path of the economy are a key driver of markets. Both higher and lower. Geopolitical risk has moved to the forefront of investors’ concerns and has become the key to that path. Prior to the beginning of this military action, news on the economy had some pluses and minuses. Economic growth remained positive. But there were certainly concerns about the future, with inflation remaining stubbornly elevated, and employment data coming in soft.

Investors became concerned that the economy would struggle to weather the impact from surging oil and gasoline prices. But Friday’s March employment data was a positive surprise with 178,000 jobs created, which was well above economist expectations. And there is reason to believe that the economy could accelerate after a weaker fourth quarter gross domestic product (GDP) print. Stimulus from last year’s One Big Beautiful Bill Act should begin to flow through the economy in combination with ongoing spending on artificial intelligence infrastructure. In my view, it is likely that the Middle East war will not push the U.S. economy into a full-blown recession.

While geopolitical risk dominates near-term headlines, valuation dynamics beneath the surface are telling a more constructive story.

Valuations Improving Under the Surface

The reason that the economic outlook is so important is because fundamentals drive markets over the long-term. But there are factors that investors should consider when making investment decisions today. The most important of which is valuations and earnings growth.

Following the April 2025 market bottom, stocks rallied strongly into 2026. This left everyone feeling better about their portfolios. But it does come with consequences. As stocks went up, valuations increased. The multiple that investors were willing to pay for forward earnings for the S&P 500 peaked at 22x.

Much like the rallies of the last few years being led by a handful of stocks, this year’s sell-off has seen similar action. The Magnificent Seven stocks (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla) are down 10% as of Friday’s close, while the other 493 stocks are basically flat. As a result, valuations have improved.

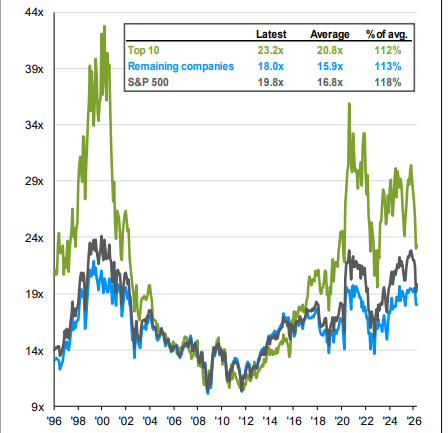

S&P 500 Valuations Are Attractive

- Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management 04/02/26

- Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results. Forward P/E ratio is the most recent price divided by the consensus estimates for earnings provided by IBES since January 1996 and FactSet since January 2022. The remaining stocks represent the rest of the 490 stocks in the S&P 500, and their P/E ratio is calculated by backing out the nominal earnings and market cap of the top 10 from that of the S&P 500.

The “S&P 500 Valuations Are Attractive” chart illustrates that the price-to-earnings (P/E) ratio for the full index is now under 20x, which is a more attractive level than a little over a month ago. Slicing the index a little differently, once we get past the names at the top of the index, the remaining 490 names are trading at just 18x earnings. Both levels are down from the beginning of the year.

This improvement, in part, reflects multiple compressions among large cap leaders. So, while valuations are improving, relatively cheap is not an investment thesis by itself.

Corporate America’s Outlook Is Improving

But what makes relatively cheap an interesting investment opportunity is improving fundamentals. Valuations could be coming down because investors expect earnings expectations to be reduced due to the impact of higher energy prices on the profit and loss statement of companies that make up the index. It certainly would not be a surprise if that is what is happening since oil prices have risen over 70% since the end of February. But that is not what is going on.

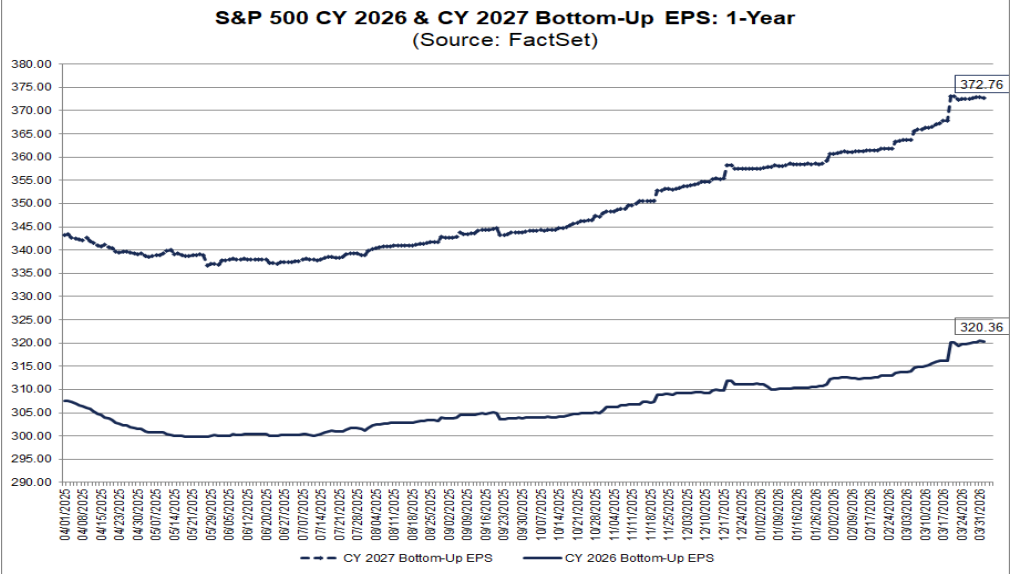

Earnings Estimates Are Actually Moving Higher

- Sources: FactSet Research 04/02/26

- Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Instead, the “Earnings Estimates Are Actually Moving Higher” chart indicates that there has been resilience in earnings expectations across the broader index. Earnings estimates have moved steadily higher over the course of March. The current estimate is now 2% higher than the February 27 FactSet estimate of $313.62. That is impressive in any environment, but a positive sign given the heightened level of geopolitical risk.

While there are risks for corporate America to navigate over the rest of 2026, if analysts’ estimates are close to right, 2026 earnings growth would be 18%. This would be on the heels of 10% growth in 2024 and 11.5% growth in 2025. Corporate America is in solid shape currently.

The final piece of the puzzle is figuring out what that means for portfolios.

Navigating the Short Term and the Long Term

While the situation in the Middle East remains fluid and until there is a resolution that opens the Strait of Hormuz that investors have confidence in, we would anticipate volatility to continue. For investors that can ignore the impact of short-term headlines, the equity market backdrop is improving.

Sell-offs will happen each year, and when they do, if there is no lasting impact on economic growth, valuations become more attractive. This time, we see improving fundamentals through rising earnings estimates. The first quarter 2026 earnings season begins in earnest next week. There is certainly the possibility that companies will take the opportunity to tamper down the enthusiasm that is being seen in analysts’ expectations. But everyone thought that would happen last year due to tariffs, and companies handily beat estimates throughout the year.

While near-term uncertainty is likely to persist, the combination of improving valuations and rising earnings expectations supports a constructive backdrop for the equity outlook. In our view, disciplined, diversified portfolios remain well positioned to navigate headwinds and participate in future market leadership.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #1089845