3.24.26 U.S. Dollar Retains Safe Haven Status

Dollar Grows Stronger

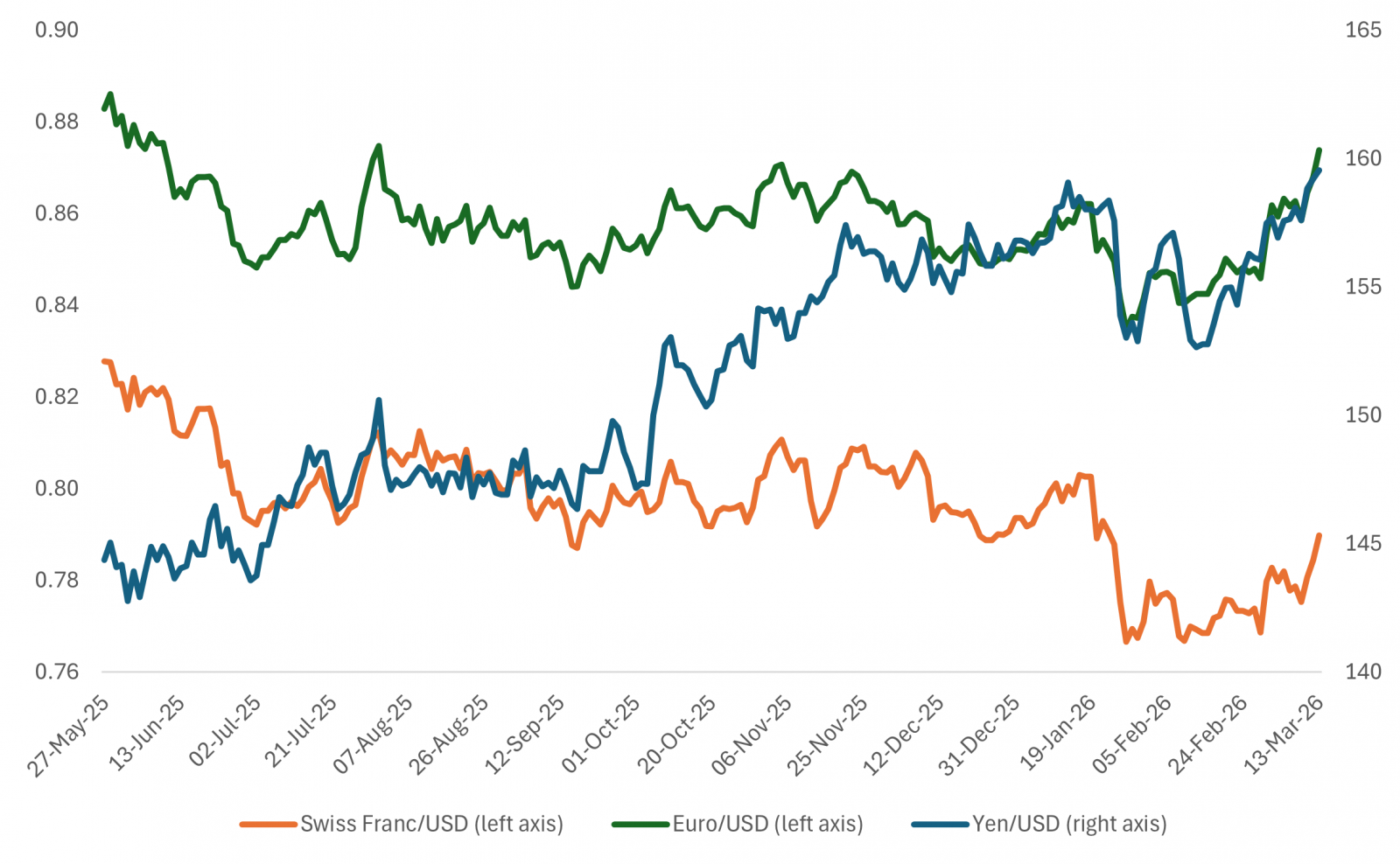

The recent appreciation of the U.S. dollar (USD) against most currencies reflects investors’ assessment that the U.S. economy offers a uniquely strong combination of relative growth resilience, higher returns, and financial-system credibility. Compared with other advanced economies, the United States continues to exhibit firmer growth, a more flexible labor market, and a Federal Reserve (Fed) committed to price stability. At the same time, global uncertainty has reinforced demand for deep, liquid dollar‑denominated assets, which remain the primary source of safe and scalable collateral. As capital flows toward the U.S. for both return and safety — and away from lower‑growth, lower‑yield, or policy‑constrained economies — the dollar strengthens broadly, signaling that global investors continue to rank the U.S. economy as a relatively safe haven.

U.S. Dollar Appreciated Across Most Currencies

- Source: LPL Research, Federal Reserve Board, 03/23/26

- Disclosures: Past performance is no guarantee of future results.

Why Has the Dollar Outperformed During the Middle East Shock?

There are some historical examples that explain why we have seen a dollar appreciation against most currencies during times of global stress. Like the 1990s, the U.S. economy has stronger relative growth and productivity than other major trading partners. The U.S. growth trajectory, for example, is stronger than in Europe and Japan. We see stronger corporate profitability and higher returns on invested capital. These factors legitimize safe‑haven flows.

Further, like the post‑Great Financial Crisis (GFC) era, we see dollar liquidity dominance. The dollar is still the primary trade invoicing unit, foreign exchange (FX) hedging benchmark, and global collateral asset. Dollar strength tightens non‑U.S. financial conditions disproportionately. As we monitor the dollar, we must keep our eyes on the Fed.

After Chair Powell Retires

If nominee Kevin Warsh is unconfirmed when Chair Powell’s term expires, Mr. Powell will most likely become Chair Pro-tempore. Fed credibility is a key factor to gauge the likely persistence of dollar performance during times of crisis, and strong leadership is necessary for maintaining credibility. The loss of the Fed's reaction-function credibility could become a powerful trigger in a regime shift in the dollar. When the Fed loses market credibility, investors no longer believe the Fed will prioritize price stability over accommodation. Or, inflation is no longer treated as mean‑reverting under the policy framework. What this looks like technically is inflation risk premia rises. The term premium steepens independently of growth, and the dollar weakens even as U.S. yields rise.

Amid global uncertainty, Fed officials need to maintain their credibility and independence.

The Tell-Tale Market Signature of a Real Regime Shift

If a dollar regime shift has started, you will observe at least these four signals. First, the USD weakens against both high‑beta and safe‑haven currencies. Second, U.S. yields rise without FX support. Third, foreign assets outperform in local currency and USD terms. Fourth, volatility rises without a flight into the dollar. Some events may give a false signal. Fed easing cycles could weaken the dollar but may not be sufficient for a real regime shift.

Given the current path of future easing, let’s end with a few counterintuitive examples of dollar strength amid lower fed funds.

U.S. rate cuts have supported the dollar at several points in history — not because lower rates are dollar‑positive mechanically, but because the cuts improved the U.S. outlook relative to the rest of the world or stabilized global risk. The key is context. Here are the cleanest examples.

First, is the 1998 Asian and Russian crisis along with Long Term Capital Management (LTCM). The Fed cut rates three times in late 1998 to contain global financial stress. The cuts stabilized U.S. growth while much of Asia and parts of Europe were in crisis. Global investors increased exposure to U.S. assets as the safest large market. The dollar strengthened despite easier policy, especially versus emerging markets (EM), and the euro’s predecessors.

The second period was the post‑dot‑com recession in 2001–2002. The Fed aggressively cut rates after the tech bust, and these cuts helped limit the depth of the U.S. downturn. Capital continued to flow into U.S. markets because alternatives were weaker. The dollar stayed strong initially and only weakened later once global growth recovered.

A third period was during the early phases of the GFC in 2008.

In the initial stage of the GFC, the Fed began cutting rates before other central banks. Markets interpreted the cuts as crisis containment, not policy weakness. The dollar rose sharply during late 2008 and 2009, even as rates fell.

However, cuts usually weaken the dollar when they signal a loss of inflation control, a fiscal or institutional breakdown, or a permanent deterioration in U.S. returns relative to the rest of the world.

Concluding Thoughts

The current appreciation of the U.S. dollar is being driven by a confluence of several factors. Here are the key drivers:

First, the U.S. economy continues to appear stronger and more adaptable than most peers, particularly Europe and Japan. U.S. consumers, labor markets, and corporate earnings have held up better, which keeps global capital oriented toward U.S. assets, even late in the cycle.

Second, U.S. central bank rates remain higher than in other advanced economies, and the Fed is viewed as more credible in maintaining price stability. That combination makes the dollar attractive, not just as a safe haven, but as a return‑generating currency.

Third, investors continue to favor assets that offer unmatched depth and liquidity. U.S. Treasuries remain the world’s primary source of scalable, high‑quality collateral, and demand for them supports the dollar even when risk sentiment deteriorates. Notably, the dollar is appreciating relative to other traditional havens like the yen and Swiss franc, reflecting a preference for liquidity and market depth over low‑yield safety.

Fourth, as a major energy producer and net exporter of petroleum products, the U.S. has benefited from relatively favorable export‑to‑import price dynamics. Stable energy prices boost U.S. real income and margins, while hurting energy‑importing economies, reinforcing dollar strength through improved relative purchasing power and resilience.

Bottom line: The dollar is strengthening because global investors see the U.S. as offering the best mix of returns, safety, and liquidity. Until one of those pillars breaks, most likely via a loss of policy credibility or a meaningful reversal in relative growth, the forces supporting dollar appreciation are likely to remain intact.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #1083018

Contact us directly should you have questions about this topic.