12.17.25 2025 Market Recap: Beyond AI and Tariffs

Much like how U.S. equity markets were driven by top-heavy artificial intelligence (AI) themes, so were many stories and headlines. For evidence of this, look no further than the recently announced 2025 Time’s Person of the Year: Architects of AI. We’ve all been fully versed this year on data centers, capital expenditure (capex), “Mag-7”, semiconductors, and the like. Not to be outdone, tariffs too, emerged as a dominant investment story, from the April Rose Garden announcement to the subsequent pause, and the ongoing impacts. Those themes, without a doubt have been cornerstones of the investment landscape, but they’ve already gotten their due. With just 10 trading days left in the year, it seems appropriate to review some less flashy, but still important developments.

Global Equity Expansion

The breadth of geographic outperformance has broadened considerably this year, with European financials and Asian tech being notable standouts. Through last week (December 12, 2025), the MSCI All Country World Index (ACWI) ex-U.S. rose 31.5%, ahead of the domestic all-cap Russell 3000 Index’s return of 17.1%. In 12 of the previous 15 years, the Russell 3000 had outperformed the MSCI ACWI Ex-U.S. Index, as evidenced in the “Foreign Equities Get Their Year” chart. A major driver of this divergence has been the weakness of the U.S. dollar (USD). Trade policy, fiscal spending (excess government borrowing), and easing monetary policy all contributed to lower demand for the greenback. As the USD slid, primarily in the first half of the year, foreign investors sought to hedge, selling dollars forward, further deepening the sell-off. That major force, combined with attractive foreign valuations, emerging market equity strength, a major German fiscal spending package, and Japanese corporate governance reforms, among other things, has certainly paid off for disciplined global investors.

Heading into 2026, our base case doesn’t include another major move down in the USD. We also expect earnings growth domestically to far outpace developed international markets, yet valuations outside the U.S. remain attractive. For these reasons and assuming the dollar holds up, we expect much more measured moves higher in foreign equities relative to U.S. equities in the year ahead.

Foreign Equities Get Their Year

- Source: LPL Financial, Bloomberg 12/12/25

- Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

Oddities Among Interest Rates

The Federal Reserve (Fed) cut rates three times in succession from September through December, trimming the target range to 3.50–3.75%. The final meeting’s 9–3 split vote, which had an abnormally high number of dissents, highlighted the ongoing debate between addressing persistent inflation and responding to signs of labor market cooling. Inflation readings were muddled by a government shutdown, but the most recent official data from September showed headline Consumer Price Index (CPI) running near 3.0% year over year, with November set to come out on December 18 (October data became a casualty of the government shutdown and won’t be available). One also can’t ignore the idea of Fed Chair Jerome Powell's waning influence on the cohesion of the Federal Open Market Committee (FOMC) as his tenure is set to end in 2026.

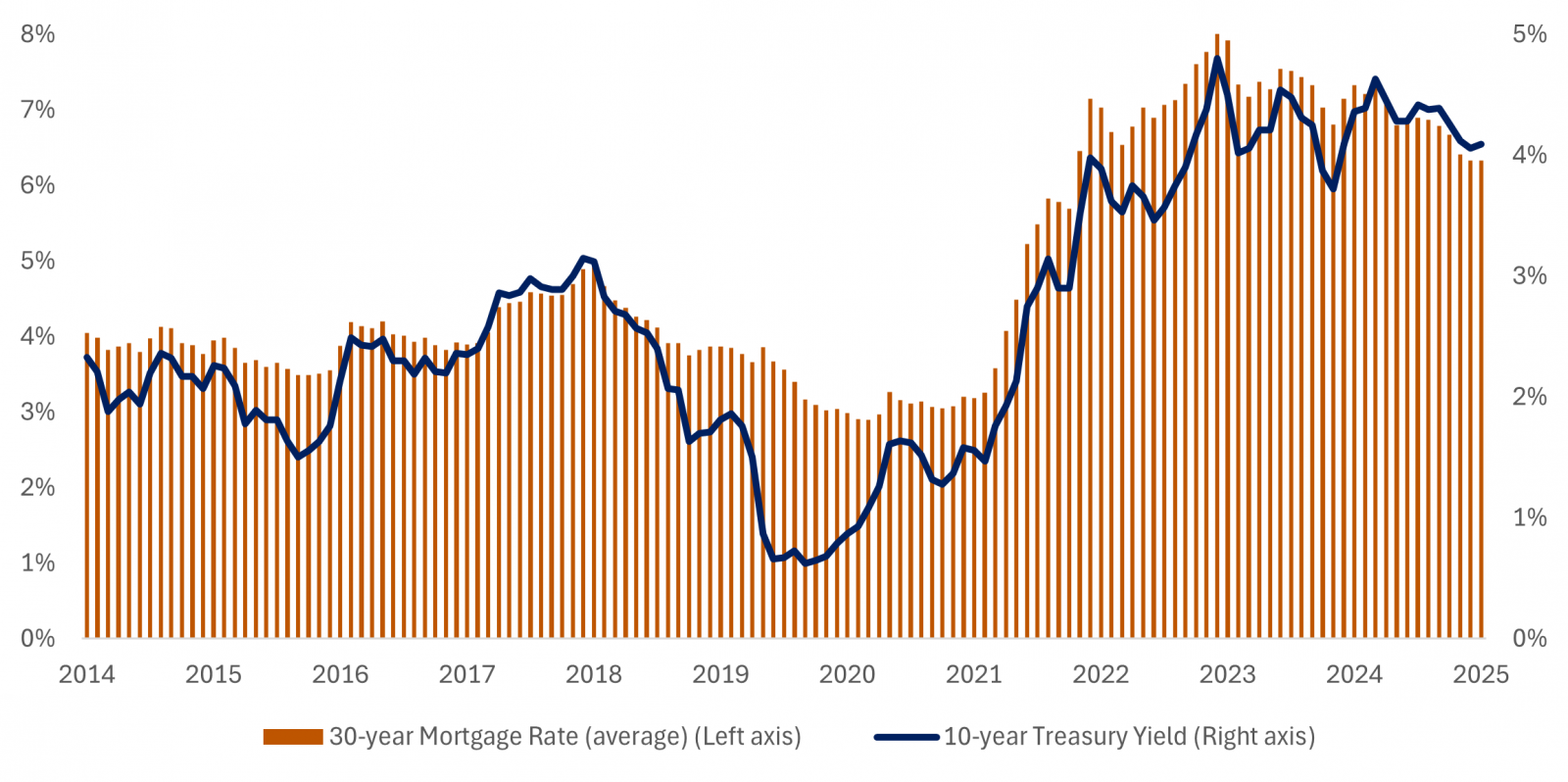

Despite the shift in policy, long-term yields told a different story. The 10-year Treasury held firm around 4.1–4.2% for much of the fourth quarter — a reflection of heavy supply, fiscal concerns, and lingering market uncertainty about inflation’s trajectory. Mortgage rates, which are more closely tied to the 10-year Treasury than the fed funds rate, eased modestly but stayed well above early-2020s levels, leaving the housing market locked up. This relationship is highlighted in the “10-Year Treasury vs. Mortgage Rates” chart. Since the Fed resumed its rate-cutting campaign in the fall of last year, completing 175 basis points (bps) of cuts, the 10-year Treasury has risen nearly half a percent, while mortgage rates have fallen marginally by about 30 bps. Volatility of interest rates has been on a substantial downward trajectory since the tariff turmoil this spring. That, combined with a softening labor market, our expected containment of inflation and normalization of the relationship between 10-year Treasury and mortgage rates, we believe, should bring home borrowing costs down to the upper-5’s by the end of next year.

10-Year Treasury vs. Mortgage Rates

- Source: LPL Research, Bloomberg, Federal Reserve Board 11/05/25

- Disclosures: Past performance is no guarantee of future results.

A Tale of Two Commodities

The story of the year in commodities has been the meteoric rise in precious metals. Gold soared to new highs above $4,300 per ounce following the Fed’s final rate cut. Not to be outshined, silver joined the rally, also marking record levels, appreciating over 114% on the year through last week. Supported by a softer dollar, declining real yields, and probably most importantly, central bank demand, we believe pullbacks in gold can be used as potential buying opportunities. A continuation of central government purchases, ETF buying pressure, and sanction-immune non-dollar reliance from foreign entities could all potentially play well in 2026.

Oil markets, on the other hand, are chugging into year-end on a weak note, with Brent crude falling below $60 per barrel this week, reaching bear market territory amid positive Russia-Ukraine peace deal developments. Global inventories have swelled, and supply growth has continued to outpace modest demand. Heading into 2026, production pauses from OPEC+ could stabilize prices, however, slower global growth, particularly in China, could stunt a meaningful rebound.

The Year Wrapped

While artificial intelligence and tariff headlines dominated the narrative in 2025, other meaningful developments unfolded as well. International equities finally broke a long streak of underperformance. At the same time, U.S. markets delivered solid gains, but with a backdrop of shifting monetary policy and unusual rate behavior — short-term cuts contrasted with stubborn long-term yields. Commodities told their own story of extremes — gold and silver soared to record highs on the back of central bank demand and macro uncertainty, while oil slipped into bear market territory amid oversupply and geopolitical progress. These divergences underscore the importance of diversification and disciplined positioning.

As we prepare for 2026, we believe the policy engine will drive returns. Policy has taken center stage as fundamentals yield to momentum and passive strategies. Markets will likely remain driven by policy shifts more so than valuations, creating heightened volatility that tests investor discipline in a tactical (shorter-term) environment. Recent swings from policy-driven lows to momentum-fueled highs underscore this dynamic, which we expect to continue. Encouragingly, policy should act as a tailwind, with monetary easing supporting growth amid contained inflation.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #838658

Contact us directly should you have questions about this topic.