11.5.25 Signs of Life in M&A

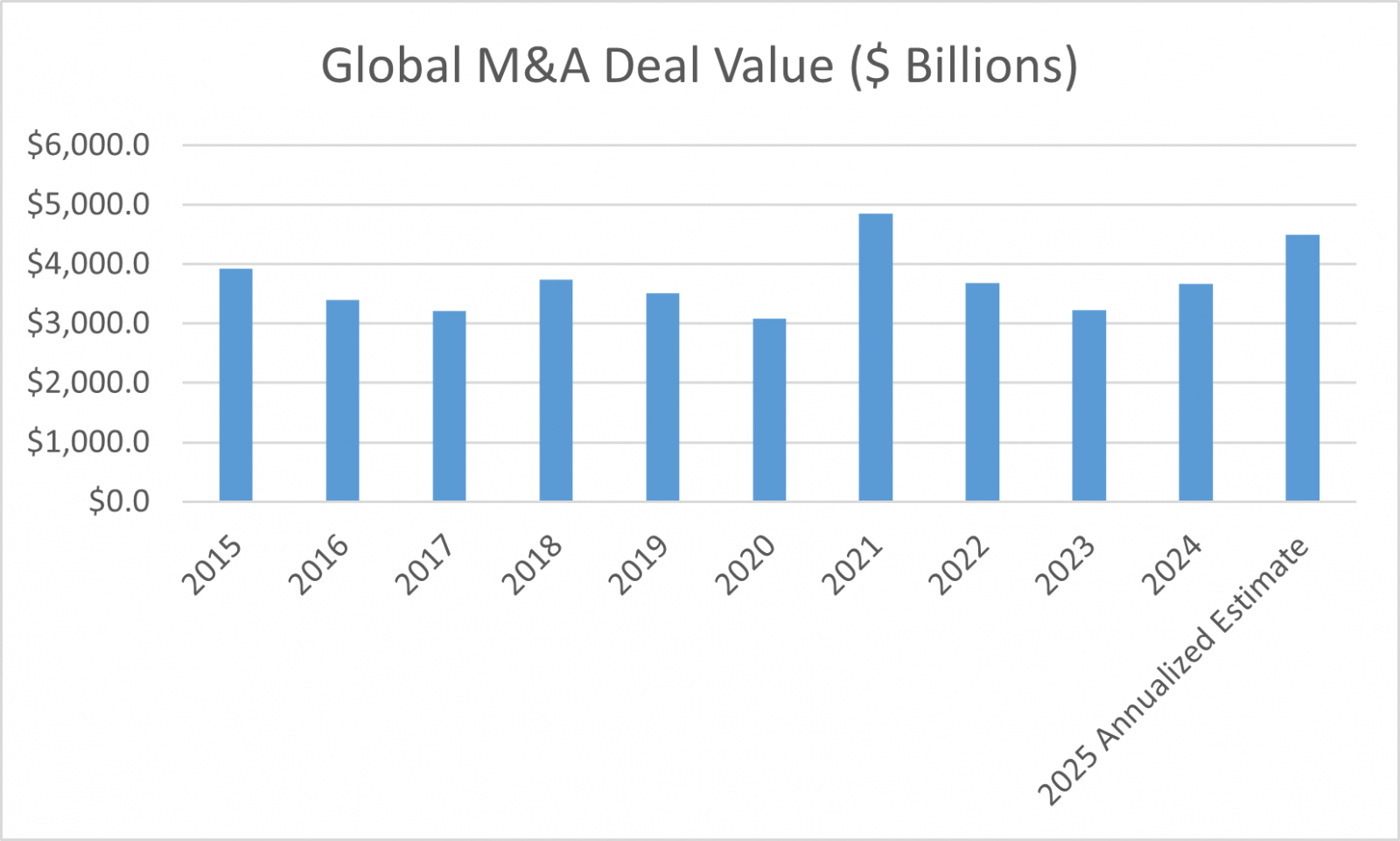

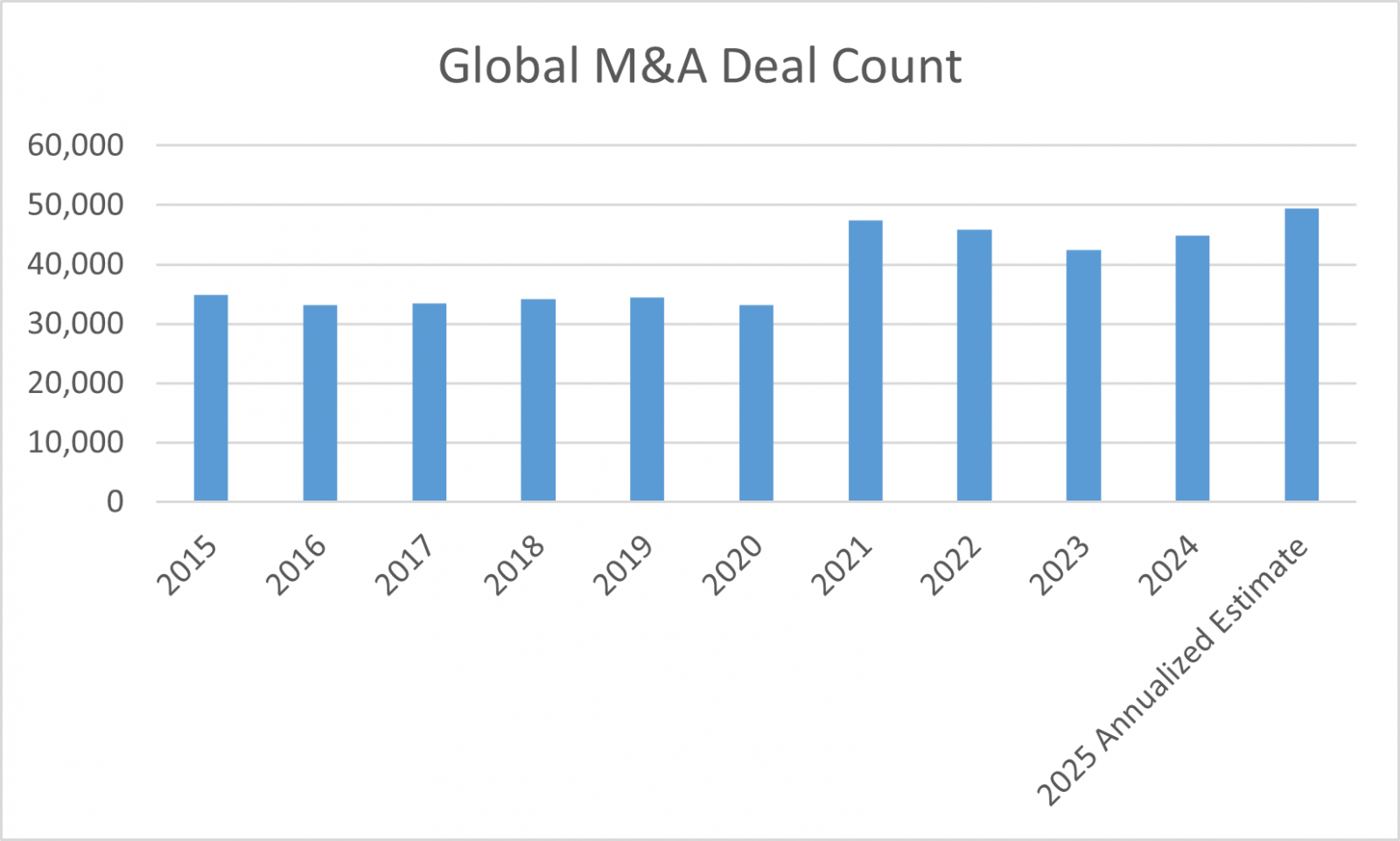

After a slow couple of years, the mergers and acquisitions (M&A) market is finally picking up momentum. According to Pitchbook, the total number of deals for the first three quarters of 2025 increased by 13% compared to the same period last year. The total deal value for the same period in 2025 reached $3.4 trillion, up 25% from the same period last year as well. The recovery we are observing is not just about the rise in the number of deals but also about the value of the deals, driven by the rise in large, strategic, sponsor-backed transactions. In terms of regions, North America continues to lead the way. While among sectors, technology continues to lead, understandably with the hype of artificial intelligence and digital transformation.

Global M&A Value Trending Higher

- Source: LPL Research, Pitchbook 09/30/25

- Disclosures: Past performance is no guarantee of future results.

Global M&A Activity on the Rise

- Source: LPL Research, Pitchbook 09/30/25

- Disclosures: Past performance is no guarantee of future results.

For merger arbitrage investors, this uptick is a welcome change. While much of the success merger arbitrage managers have shown this year is the result of announced deal spreads tightening due to the strength in equity markets, the rebound in M&A activity will serve as an additional tailwind for the coming quarters. Simply put, there just were not enough deals to build a diversified book for the last couple of years, and many spreads were too tight to justify the risk. Now, bigger and more complex transactions are creating more opportunities. Spreads remain attractive as well, in part because markets are still pricing in regulatory and financing uncertainty.

Private equity has finally gotten a bit of a break, too. After years of slow exits and few chances to deploy capital, sponsors are once again able to find both buyers and sellers. The value of exit deals has climbed 18% year over year and the number of exits also rose approximately 9%, pointing to a broader and deeper pipeline of realizations taking shape. That momentum has allowed general partners to recycle capital and finally begin to deliver the long-awaited distributions to limited partners, even though some of the key metrics remain below their long-term averages.

Overall, it is too early to call this a full-fledged recovery and there still are many roadblocks — inflation remains stubborn in parts of the economy, rate cut expectations could be disappointed, and trade uncertainty still lingers. Still, the change in tone is unmistakable. The M&A market is not back to full speed, but we believe it’s moving in the right direction.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #821087

Contact us directly should you have questions about this topic.