11.13.24 Are Tariffs Always Inflationary

Key Talking Points

• Reported this morning, October inflation rose 0.2% from a month ago, the same monthly pace as July, August, and September as inflation is finding its balance.

• Despite the fairly steady monthly pace of inflation, the annual rate rose to 2.6% and is attributed to abnormal and large declines in gas prices back in October 2023. It does not appear to be signaling a new trend but rather base effects.

• The sticky components of inflation continue to ease, giving the Fed some leeway to cut rates next month, but they could pause in January. The strength of some cohorts of the consumer is keeping upward pressure on prices and stronger-than-expected economic growth is likely keeping bond yields elevated.

• But most importantly, markets seem preoccupied with the inflationary impact from rogue tariffs. From lessons learned during the 2018 tariffs, consumer prices may not reflect the full cost of a tariff, although somebody must bear the burden.

Finding Steady State

Several categories of consumer prices appear to be entering their steady state. Now with October data, we have four consecutive months where headline inflation rose 0.2%. Excluding car prices, core goods prices fell and services, less shelter, decelerated.

One of the most debated components to measure consumer inflation is Owners’ Equivalent Rent (OER), which has a 27% weight in the Consumer Price Index (CPI). OER is an imputed value of what homeowners would hypothetically have to pay for their home if they were renters and not owners.

Fed Set to Cut

The cooling of the labor market, the easing of the important components of inflation, and tight monetary policy will incentivize the Federal Open Market Committee (FOMC) to cut rates by 25 basis points (0.25 of a percentage point) at the December meeting but could prepare investors for their inclination to pause in January.

What Really Matters Are Tariffs

Investors are preoccupied — and rightfully so — with inflation risks from tariffs. As the International Trade Administration thoroughly explains, a tariff is a tax on the customs value of an imported product. Who bears the cost of the tax? It’s not always fully borne by end consumers. According to a National Bureau of Economic Research (NBER) paper, foreign countries bore “close to half the cost of the steel tariffs.”1 Of course, there are two very important considerations to include in the analysis: exclusions and item-specific markets.

During Trump’s first presidency, he granted exclusions for over 2,200 products based on businesses’ defense that the tariff causes considerable harm, or the foreign product is not available in the U.S. Ironically, Biden kept most of Trump’s tariffs and put additional tariffs in place in May of this year.2

What Happened to Inflation in 2018–2019?

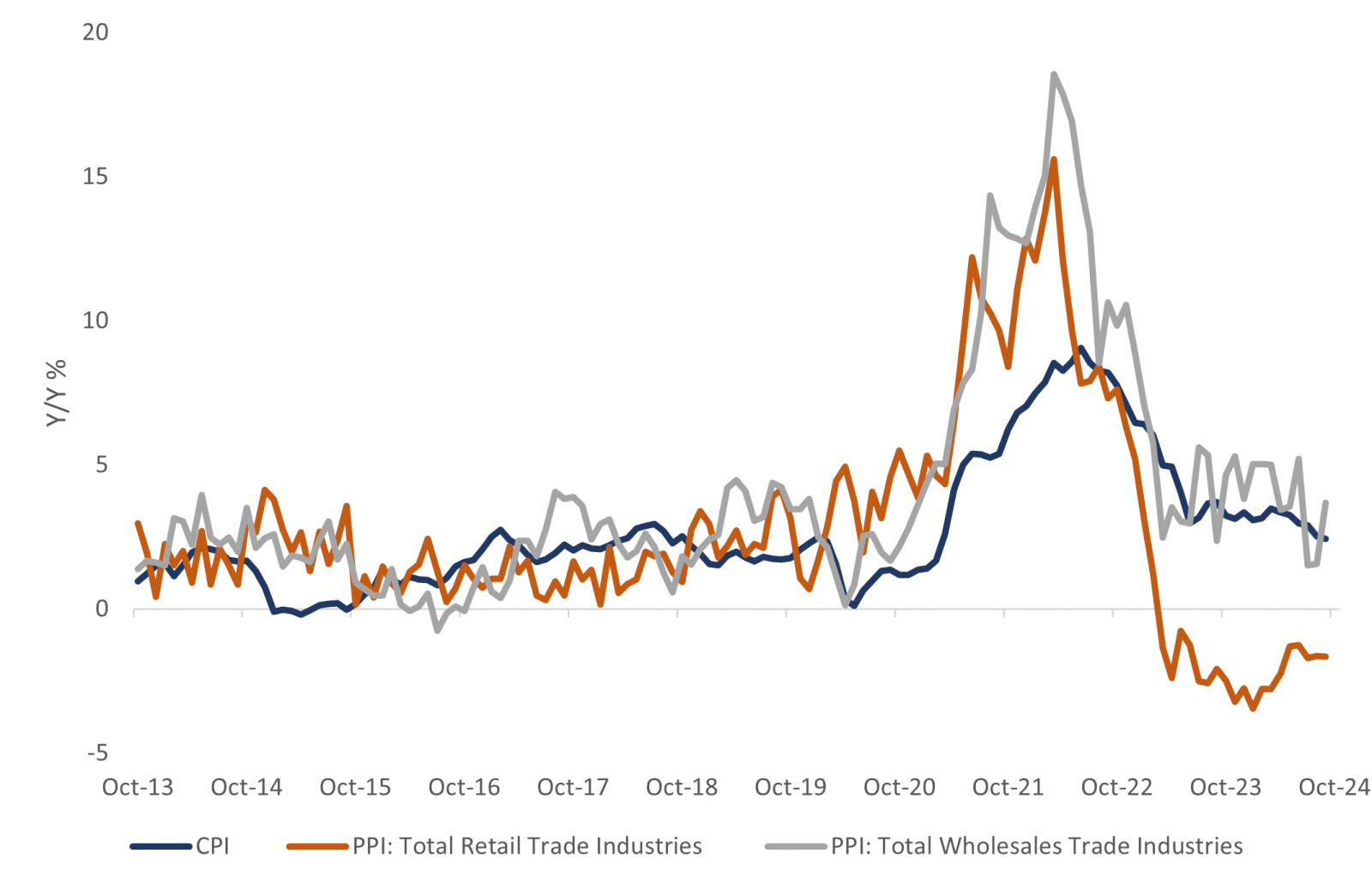

In this blog, we notice that tariffs imposed in early 2018 impacted producer prices more than consumer prices as wholesalers did not fully pass along the cost of importing

Wholesalers Didn't Fully Pass Along Tariffs of 2018–2019

- Source: LPL Research, Bureau of Labor Statistics, 11/12/2024 Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

Summary

In general, a tax from tariffs, or any other policy, creates a deadweight loss to the economy. Businesses and consumers feel the impact; employment typically shrinks, and our foreign trading partners often retaliate. Among the possible positive impacts from these types of trade actions are negotiating opportunities, shifts toward more domestic production, and maybe some humanitarian improvements as well. Maybe trade threats could punish foreign businesses who exploit their workers with inhumane working conditions. We could hope the world becomes a safer and fairer place, even for workers in other parts of the globe.

As it relates to the investment outlook, markets are right to have caution as we enter 2025. There are economic headwinds, but so far, a stable consumer, looser Fed policy, and businesses planning to ramp up capital expenditures may keep supporting this market. Caveat emptor.

- 1 https://www.nber.org/papers/w26610

- 2 https://taxfoundation.org/research/all/federal/trump-tariffs-biden-tariffs/

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- Tracking: #657758