11.25.25 Japanese Stimulus Tests Yields and the Yen

Last week’s artificial intelligence (AI) led global equity rout captivated headlines, overshadowing notable developments flowing out of Tokyo. Recently elected Japanese Prime Minister Sanae Takaichi — the pro-growth and pro-stimulus policy lawmaker — and her cabinet approved the country’s largest stimulus package since the pandemic on Friday, totaling 21.3 trillion yen ($135 billion). The announced 17.7 trillion-yen ($112 billion) spending plan is primarily aimed at price relief for citizens and features a three-month gas and electricity subsidy for each household, a cash handout for children, a reduced gasoline tax, and an increased tax-free income ceiling. Public support for the cabinet remains strong, but the Takaichi administration is faced with walking a tightrope: balancing between appealing to voters’ frustrations with sticky inflation, while not unsettling investor scrutiny of the country’s fiscal position and keeping the debt burden in check to stave off bond vigilantes.

Markets Show Some Unease Toward the Package

While the Cabinet Office estimates that the price measures will reduce inflation by an average of 0.7% from February to April next year, the market has shown signs of concern about the package. Japanese government bond (JGB) yields surged ahead of the announcement due to unease that Takaichi (a former mentee and so-called disciple of Shinzo Abe, father of early 2010s expansionary policy reform, ‘Abenomics’) is implementing an aggressive version of Abenomics at a time when debt markets might not be able to handle increased debt issuance. A fair consideration given gross government debt comprises 230% of GDP — the largest among advanced economies (nearly double the 125% U.S. debt burden, for perspective).

Simultaneously, friction between the administration and central bankers has increased market angst. Inflation has remained above the Bank of Japan’s (BOJ) target level for over three years, and consumption has grown sluggish as a result. Investors expected a rate hike to help tame inflation at the upcoming December meeting, but market pricing for a potential hike tumbled last week as markets acknowledged fears from Prime Minister Takaichi and her cabinet that premature tightening could spoil their plans to rejuvenate economic growth. The resulting skepticism that the BOJ can tighten monetary policy fast enough to combat inflation is also a driving factor of the spike in JGB yields, while concerns of BOJ credibility are on the rise.

Japanese Yields Surge on Stimulus Package

- Source: LPL Research, Bloomberg 11/24/25

- Disclosures: Past performance is no guarantee of future results.

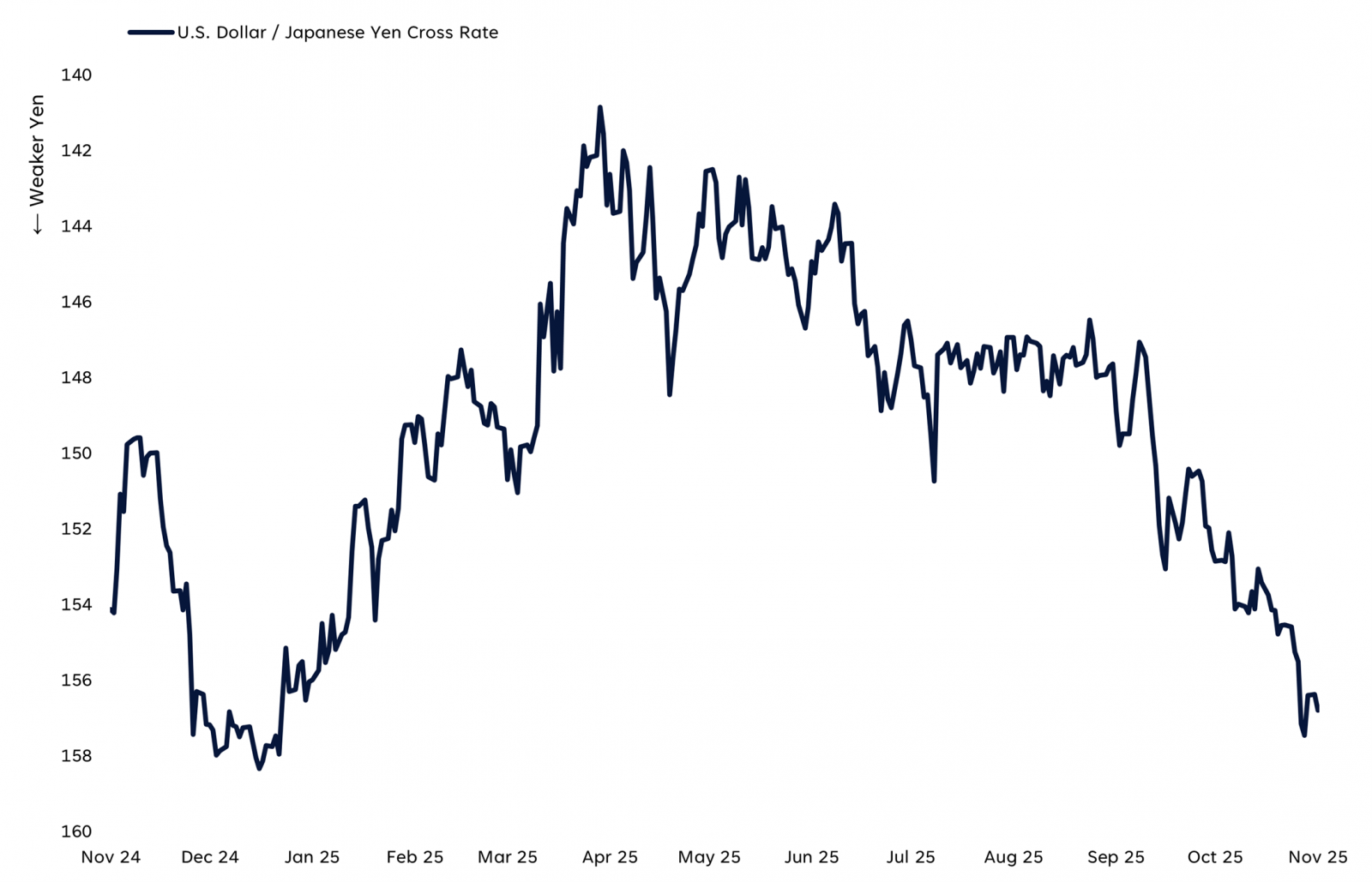

Adding another layer of complexity to market dynamics around the stimulus package is the yen. Worries around the government’s hand in monetary policy and the increased debt burden have caught the yen between the two factors, sending the currency near its lowest levels since January. As a rule of thumb laid out by previous currency chief Masato Kanda in 2024, a 10-yen move against the dollar within a month is what central bankers consider rapid. The yen’s one-month move against the dollar reached as high as 6.7-yen last week, before receiving support after Finance Minister Satsuki Katayama stated that currency intervention remains on the table. Although, strength was short lived as the currency has since resumed its move lower. The BOJ is likely to fulfill hopes of a rate hike in the coming months but waiting until January will likely expose the yen to additional downward pressure while increasing the potential for Tokyo to intervene. However, Japan’s ability to step in is capped with Tokyo relying on foreign exchange reserves to back around 50% of its $550 billion investment in U.S. funds.

Yen Weighed Down by Monetary and Fiscal Jitters

- Source: LPL Research, Bloomberg 11/24/25

- Disclosures: Past performance is no guarantee of future results.

Conclusion

The Japanese economy may need the stimulus after recent data indicated core and headline inflation ticked higher last month, while gross domestic product (GDP) contracted 1.8% last quarter — marking the first decline in six quarters. But investors clearly have questions on whether capital markets and Tokyo can handle the additional spending and the conflicting dynamics between lawmakers and policymakers. The coming weeks will test the yen and JGB yields, as well as the Takaichi administration, which also faces its first real test of how long her new government can last via the diplomatic tensions with China. Plus, effects could spill overseas, as an extension of the rise in JGB yields could add upward pressure on U.S. Treasuries, for example. Last week’s developments don’t indicate the start of a dire situation, but when equity markets, bonds, and currencies fall in concert, it’s rarely a good mix.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) remains neutral on developed international equities, which includes the Eurozone and Japan. Valuations, while still reasonable, have risen, and U.S. dollar weakness is far from assured. Debt and defense spending in Europe helps, but U.S. tech strength is tough to match.

- Important Disclosures

- This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

- Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

- Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

- This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

- Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

- Asset Class Disclosures –

- International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

- Bonds are subject to market and interest rate risk if sold prior to maturity.

- Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

- Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

- Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

- Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

- High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

- Precious metal investing involves greater fluctuation and potential for losses.

- The fast price swings of commodities will result in significant volatility in an investor's holdings.

- This research material has been prepared by LPL Financial LLC.

- Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

- For Public Use – Tracking: #830353

Contact us directly should you have questions about this topic.